International Monetary Fund (IMF) Managing Director Kristalina Georgieva speaks at a press conference in Washington D.C., the United States, on March 4, 2020. (LIU JIE / XINHUA)

International Monetary Fund (IMF) Managing Director Kristalina Georgieva speaks at a press conference in Washington D.C., the United States, on March 4, 2020. (LIU JIE / XINHUA)

WASHINGTON - The guardians of the global economy are warning that the recovery from this year’s recession is at risk and could be derailed as the resurgence of COVID-19 forces fresh restrictions on households and companies.

Both the International Monetary Fund and the Group of 20 -- which comprises the world’s richest nations -- sounded the alert as leaders of the G-20 prepare for a virtual summit this weekend, hosted by Saudi Arabia.

Both the International Monetary Fund and the Group of 20 -- which comprises the world’s richest nations -- sounded the alert as leaders of the G-20 prepare for a virtual summit this weekend, hosted by Saudi Arabia

The IMF noted progress on a vaccine, but also said elevated asset prices point to a disconnect from the real economy and a potential threat to financial stability.

“While global economic activity has picked up since June, there are signs that the recovery may be losing momentum, and the crisis is likely to leave deep, unequal scars,” officials at the Washington-based fund said in a report published Thursday. “Uncertainty and risks are exceptionally high.”

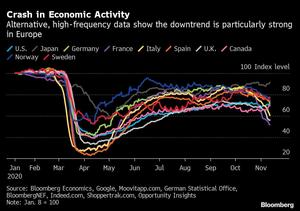

The UK, Germany and France as well as parts of the US and Australia are among those with new curbs on movement and businesses to contain the pandemic. They’re not as stringent as the lockdowns imposed earlier in the year, but are still enough to damage growth.

ALSO READ: IMF cuts Asia's growth forecast, warns of pandemic-driven risks

“We are determined to continue to use all available policy tools as long as required to safeguard people’s lives, jobs and incomes, support the global economic recovery, and enhance the resilience of the financial system.”

The final wording could still change after the virtual meeting.

A Bloomberg Economics index of high-frequency data shows activity contracting since the middle of last month. It previously began a rapid recovery in May that petered out at about 80 percent of its normal level in July.

“Countries have started to climb back from the depths of the COVID-19 crisis,” IMF Managing Director Kristalina Georgieva said in a blog post. “But the resurgence in infections in many economies shows just how difficult and uncertain this ascent will be.”

ALSO READ: IMF: Mideast, Central Asia may see decade of economic pain

The fund urged governments and central banks not to prematurely withdraw policy support. The Federal Reserve and European Central Bank are debating further stimulus as soon as next month even amid mounting confidence that a vaccine for the virus is nearing.

Georgieva said some economies have room for greater fiscal support next year beyond current budgets, and warned against cutting off lifelines such as expanded unemployment benefits.

But talks over another stimulus package among US politicians seem to have stalled and some previous measures are set to expire. In Europe, a massive recovery fund is at risk because of disagreements over conditions.

The IMF last month warned that the world economy still faces an uneven recovery until the virus is tamed. At the time, it cut its prediction for the slump this year to 4.4 percent from the 5.2 percent drop seen in June, though that would still be the deepest contraction since the 1930s.

Georgieva encouraged G-20 nations to prepare synchronized infrastructure investments once the virus is better controlled, saying that new IMF research shows large economic gains from such spending. Should countries act alone, it would take about two-thirds more spending to achieve the same outcomes, she said.

The head of the World Health Organization (WHO) on Monday said G20 leaders had an opportunity to commit financially and politically to the COVAX global facility, set up to provide COVID-19 vaccines to poorer countries.

READ MORE: IMF chief: China growth positive impulse for world economy

The United States, under outgoing President Donald Trump, has threatened to pull out of the WHO, and has refused to join the COVAX facility, but experts say his successor, Democrat Joe Biden, could change course after he takes office on Jan 20.

Georgieva also called on G20 leaders to commit to increased investment in green technologies and increases in carbon prices, estimating that doing so could boost global gross domestic product and create about 12 million jobs over a decade.

Biden has also pledged to rejoin the 2015 Paris climate change agreement that Trump quit.

With inputs from Reuters